A life settlement review is a formal assessment process where a CPA or financial advisor analyzes a client’s permanent life insurance policy for potential sale value in the secondary market, typically yielding far more than the policy’s cash surrender value. The Life Insurance Settlement Association reports that sellers have received on average 6.5 times cash surrender value through settlements. That gap between surrender value and market value is precisely why CPAs recommend life settlement review as a standard step before any policy is surrendered or lapsed. For clients holding permanent policies with face values above $100,000, skipping this review is not a neutral decision. It is a financial loss waiting to happen.

Why CPAs recommend life settlement review before policy surrender

The core reason CPAs and financial professionals initiate life settlement reviews is straightforward: settlement bids can yield significantly more cash than surrendering a policy, and if no bids materialize, the client simply proceeds with the surrender. There is no downside to looking.

The mechanics matter here. When a client surrenders a policy, the insurance carrier pays the accumulated cash surrender value and the relationship ends. When a client sells through the secondary market, an institutional buyer pays a lump sum based on the policy’s death benefit, the insured’s life expectancy, and current premium obligations. That lump sum is almost always larger than the surrender value because the buyer is pricing the eventual death benefit, not just the accumulated cash.

The competitive bidding process amplifies this advantage. A qualified broker submits the policy to multiple buyers simultaneously, creating a marketplace where buyers compete for the asset. This competition directly benefits your client. A single carrier quote at surrender has no such competitive pressure.

Life settlements also transfer future premium obligations to the buyer, which addresses a second financial problem many clients face. Seniors on fixed incomes who can no longer afford premiums often lapse policies entirely, receiving nothing. A settlement converts that liability into immediate liquidity.

-

Settlement proceeds can fund long-term care costs, retirement income gaps, or estate planning needs

-

Premium relief frees up recurring cash flow for clients on fixed incomes

-

The review itself costs clients nothing, since broker fees are paid from proceeds and are typically capped by statute

-

Multiple bids create a competitive marketplace that maximizes fair compensation

Pro Tip: Before a client signs any surrender paperwork, run a preliminary eligibility check. The review costs nothing and takes days. The opportunity cost of skipping it can reach six figures.

What policies qualify for a life settlement review

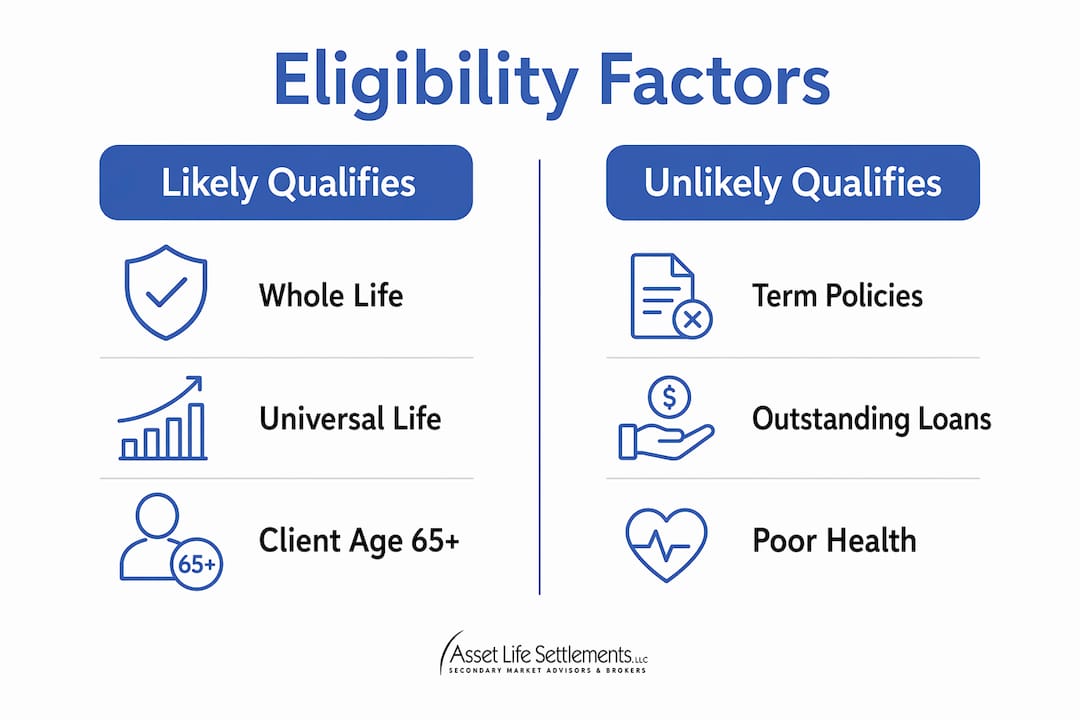

Not every policy belongs in a settlement review, and CPAs who understand the eligibility criteria can focus their time on clients where the analysis will actually produce results. Term policies typically do not qualify, and policies with face values under $100,000 rarely attract competitive bids. The review is most productive for permanent policies held by clients aged 65 or older with documented health changes since the policy was issued.

The table below summarizes the key eligibility factors CPAs use when conducting an initial policy screen.

| Factor | Likely qualifies | Unlikely to qualify |

|---|---|---|

| Policy type | Whole life, universal life, variable universal life | Term life (unless convertible) |

| Face value | $100,000 or more | Under $100,000 |

| Insured age | 65 or older | Under 65 in good health |

| Health status | Declined since policy issue | Excellent, no changes |

| Premium burden | High relative to client income | Manageable, client wants coverage |

Client health is a particularly important variable. A buyer prices the policy based on life expectancy. A client whose health has declined since the policy was issued presents a shorter expected premium payment period for the buyer, which increases the settlement offer. CPAs working with clients who have received a serious diagnosis should treat a settlement review as a priority step, not an afterthought.

There are also situations where a review is unnecessary. If a client has outstanding policy loans that have eroded the death benefit, or if existing riders already fulfill the client’s liquidity needs, the settlement may offer limited additional value. The life settlement eligibility analysis should always weigh what the client already has against what the market would pay.

How CPAs handle the tax and compliance side of life settlements

Life settlement transactions carry specific IRS reporting obligations, and CPAs play a central role in making sure those obligations are met correctly. IRS Form 1099-LS is issued by the settlement buyer and reports the gross proceeds to the IRS. A second form, 1099-SB, is issued by the insurance carrier and reports the policy’s investment in contract. Both forms feed into a three-tier taxation structure that CPAs must apply correctly.

The three tiers work as follows:

-

Return of basis. The portion of proceeds equal to total premiums paid is tax-free. This is the client’s cost basis in the policy.

-

Ordinary income. Proceeds above basis up to the policy’s cash surrender value are taxed as ordinary income, the same treatment as a policy surrender.

-

Capital gains. Proceeds above the cash surrender value are taxed at long-term capital gains rates, assuming the policy was held for more than one year.

Misclassifying the second and third tiers is a common filing error, particularly when tax software auto-populates fields from the 1099-LS without accounting for the cash surrender value threshold. CPAs who build defensible filing records by assembling the policy basis, the carrier’s cash surrender value statement, and the settlement agreement into a single documentation package reduce audit exposure significantly.

The advisory value extends beyond the tax return itself. Scenario modeling that shows a client the after-tax net proceeds from a settlement versus the after-tax value of surrendering or lapsing the policy is the kind of documented advice that demonstrates fiduciary care and protects the advisor if questions arise later.

Pro Tip: Request the carrier’s in-force illustration showing the current cash surrender value before the settlement closes. This figure is the dividing line between ordinary income and capital gains treatment, and having it documented before filing removes ambiguity entirely.

What advisors miss when they skip life settlement reviews

The scale of missed opportunity in this market is significant. Approximately $50 billion in potentially eligible life insurance policies are surrendered or lapsed annually without the policyholder ever being told a secondary market exists. That figure represents real client wealth that advisors failed to protect.

The regulatory environment is shifting in response. Life settlements are regulated in 43 states, and in some jurisdictions, carriers are required to disclose the settlement option at the point of surrender. In states without mandatory carrier disclosure, the obligation falls on the fiduciary advisor. Raising the settlement option before a policy lapses is increasingly viewed as a duty of care, not an optional conversation.

“The advisory value is in scenario modeling and documenting a client’s tradeoffs among liquidity, taxes, and lost death benefit protection.” — The Daily Upside

Major broker-dealers have updated their guidance to reflect this shift. FINRA has issued guidance encouraging advisors to consider life settlements as part of their review of client insurance holdings. CPAs who stay current on FINRA’s guidance on life settlements are better positioned to advise clients within the evolving regulatory framework.

The practical steps for proactive advisors include:

-

Review client insurance holdings annually, not only at the point of surrender

-

Flag policies held by clients aged 65 or older with permanent coverage above $100,000

-

Document the conversation where you raised the settlement option, even if the client declines

-

Partner with a licensed life settlement broker to obtain actual market bids before advising on surrender

The documentation point deserves emphasis. Advisors who ethically introduce life settlements to clients and record that conversation have a clear record of fulfilling their duty of care. Advisors who do not raise the option have no such protection.

Key takeaways

A life settlement review is the single most effective step a CPA can take to protect client asset value before a permanent life insurance policy is surrendered or lapsed.

| Point | Details |

|---|---|

| Secondary market value | Sellers receive on average 6.5 times cash surrender value through competitive settlement bids. |

| No-cost review | Broker fees come from proceeds and are capped by statute, removing any financial barrier to reviewing. |

| Tax complexity requires CPA expertise | Three-tier taxation on proceeds requires careful documentation of basis, CSV, and settlement agreements. |

| Fiduciary duty is clear | In states without mandatory carrier disclosure, raising the settlement option is the advisor’s duty of care. |

| Eligibility screening saves time | Focus reviews on permanent policies above $100,000 held by clients aged 65 or older with health changes. |

Why I think most CPAs are still underusing this tool

I have worked with financial professionals across a wide range of client scenarios, and the pattern I see most often is not negligence. It is unfamiliarity. CPAs who are deeply competent in tax strategy and financial planning simply were not trained on life settlements, and the secondary market has historically been opaque enough that the gap never felt urgent.

That is changing. The combination of regulatory pressure, documented fiduciary risk, and a market that now routinely returns multiples of surrender value has moved life settlement reviews from a niche option to a standard planning step. The advisors I respect most have started treating it the way they treat Roth conversion analysis: a scenario you run before making an irreversible decision, not after.

The conversation with clients does not need to be complicated. Something as direct as “Before we surrender this policy, let me check whether the secondary market would pay you more” takes thirty seconds and opens a door that could be worth tens of thousands of dollars to your client. The scenario modeling that follows, showing after-tax proceeds across surrender, settlement, and lapse scenarios, is where your expertise as a CPA adds real value that no broker or carrier representative can replicate.

The one caution I would offer is this: do not let the tax complexity become a reason to avoid the conversation. Yes, the three-tier treatment requires careful documentation. Yes, the 1099-LS and 1099-SB forms require attention. But that complexity is exactly why your clients need a CPA at the table when they consider a settlement. It is not a reason to stay out of the conversation. It is the reason you belong in it.

— Scott Thomas

How Asset Life Settlements supports CPAs in the review process

Asset Life Settlements works directly with CPAs and financial professionals to make life settlement reviews a practical part of client consultations, not a complicated detour.

The team at Asset Life Settlements handles eligibility analysis, policy submission to multiple buyers, and bid management, so you can focus on advising your client on the financial and tax implications rather than managing the transaction. Their life settlement process is built for financial professionals who need a transparent, documented workflow they can stand behind. For CPAs who want to build this capability into their practice, the resources for financial professionals at Asset Life Settlements provide the tools and support to get started. Reach out to learn how a partnership with Asset Life Settlements can help you deliver better outcomes for your clients.

FAQ

What is a life settlement review?

A life settlement review is an assessment of a client’s permanent life insurance policy to determine whether it has secondary market value exceeding its cash surrender value. The review involves submitting the policy to licensed buyers for competitive bids before any surrender decision is made.

Why do CPAs recommend life settlement reviews for seniors?

CPAs recommend reviews for seniors because clients aged 65 or older with permanent policies above $100,000 are most likely to receive competitive bids, and the proceeds can fund retirement income, long-term care, or estate planning needs that surrender values alone cannot support.

How are life settlement proceeds taxed?

Proceeds are taxed in three tiers: return of premiums paid is tax-free, amounts above basis up to cash surrender value are ordinary income, and amounts above cash surrender value are taxed at capital gains rates. IRS Form 1099-LS reports gross proceeds and must be reconciled against the policy’s cost basis.

Does a life settlement review cost the client anything?

No. Broker fees are paid from settlement proceeds and are typically capped by state statute, making the review a no-cost exploratory step for the client.

What is the CPA’s fiduciary duty regarding life settlements?

In states without mandatory carrier disclosure, fiduciary advisors are expected to raise the settlement option before a policy lapses or is surrendered. Documenting that conversation is part of fulfilling the duty of care under the current regulatory framework covering 43 states.