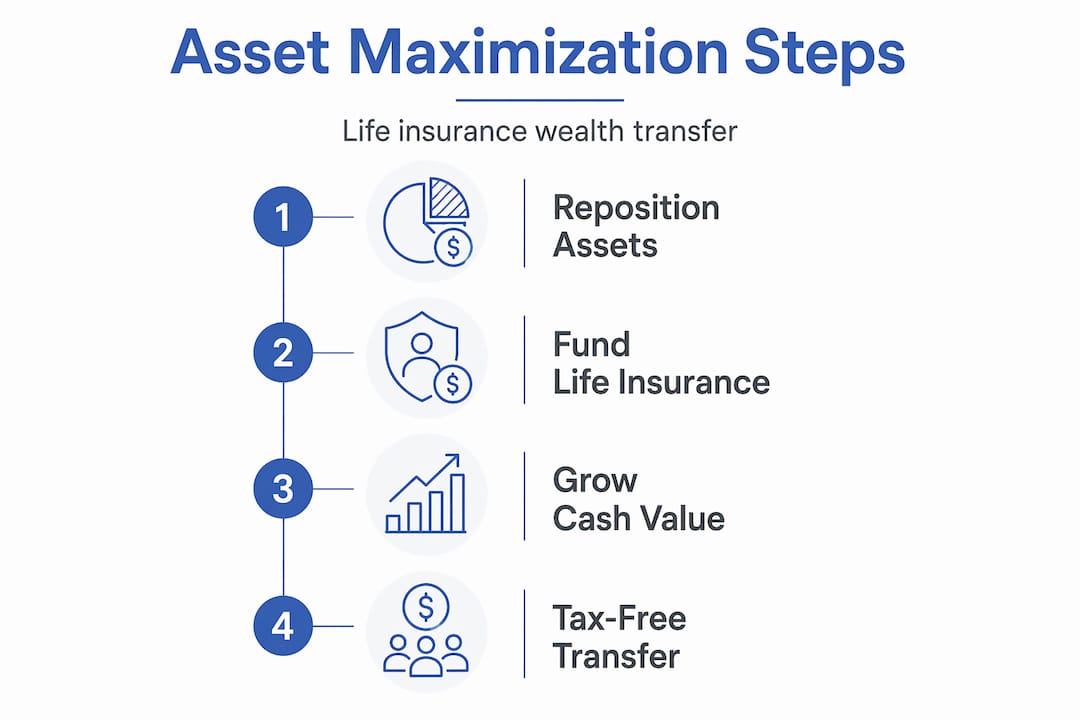

Most people think of life insurance as a safety net that pays out when someone dies. That framing is accurate but incomplete. What is life insurance asset maximization? It’s the practice of treating your permanent life insurance policy as a living, growing financial asset rather than a passive expense. Done right, it generates tax-advantaged wealth, provides liquidity during your lifetime, and transfers value to your heirs far more efficiently than most conventional investments. This article breaks down how it works, who benefits, and how to put it into practice.

Table of Contents

Key takeaways

| Point | Details |

|---|---|

| Life insurance as an asset | Permanent policies build cash value that grows tax-deferred and can be accessed during your lifetime. |

| Tax efficiency matters | Life insurance can deliver after-tax equivalent returns of 8–12%, outperforming many taxable fixed-income options. |

| Timing affects outcomes | Delaying coverage increases premiums and limits your options; starting early preserves both affordability and flexibility. |

| Annuity repositioning works | Converting a deferred annuity into a SPIA that funds a life insurance policy can significantly increase what heirs receive. |

| Life settlements add value | Selling a policy on the secondary market can yield far more than surrendering it back to the insurer. |

What is life insurance asset maximization?

Understanding life insurance starts with recognizing that not all policies are built the same. Term insurance is pure protection. It covers a set period, builds no cash value, and expires. Permanent life insurance is a different tool entirely.

Whole life, universal life, and variable universal life policies all share one defining feature: a cash value component that grows over time. That growth is tax-deferred, meaning you don’t pay taxes on gains as they accumulate inside the policy. This is the foundation of life insurance asset maximization. You’re not just buying a death benefit. You’re building a financial asset that compounds inside a tax-advantaged structure.

Here’s what permanent life insurance can do that term cannot:

-

Build cash value that grows at a guaranteed or market-linked rate, depending on the policy type

-

Provide liquidity through policy loans or withdrawals, which you can access without triggering a taxable event in most cases

-

Serve as collateral for business or personal loans, giving you borrowing power without liquidating investments

-

Deliver a death benefit that is typically received income-tax-free by your beneficiaries

Cash value grows tax-deferred inside the policy, and loans against that value reduce the death benefit only if left unpaid. Withdrawals that exceed your cost basis may trigger taxes, so working with a financial professional matters. The key point is that this cash value is a real, accessible asset, not a number that only materializes at death.

Variable universal life policies add a layer of market exposure through investment sub-accounts, offering growth potential tied to equities. Whole life policies offer more predictable, guaranteed growth. Universal life sits between the two, with flexible premiums and adjustable death benefits. Each has a place depending on your goals, risk tolerance, and timeline.

Core benefits of asset maximizing strategies

The reason financial planners increasingly recommend life insurance as part of a wealth strategy comes down to one word: efficiency. Life insurance moves assets into a structure where they grow without annual tax drag, pay out tax-free, and can be repositioned to serve multiple financial goals at once.

Here’s how asset maximization strategies compare to standard taxable alternatives:

| Strategy | Tax on growth | Tax on payout | Liquidity | Estate benefit |

|---|---|---|---|---|

| Taxable investment account | Annual (capital gains/dividends) | Yes | High | Included in estate |

| Fixed annuity | Tax-deferred | Ordinary income | Limited | Taxable to heirs |

| Permanent life insurance | Tax-deferred | Tax-free (death benefit) | Moderate (loans/withdrawals) | Passes outside probate |

Life insurance acts as a tax-efficient wrapper that shifts assets from taxable environments to reduce the total tax drag on your portfolio. Financial advisors call this “asset location.” Rather than holding bonds or CDs in a taxable account where interest is taxed every year, you reposition those assets into a permanent policy where the same growth compounds untouched.

Life insurance also solves a problem that many families don’t anticipate: illiquid estates. If your wealth is tied up in a family business, real estate, or other hard-to-sell assets, your heirs may face a forced sale just to cover estate taxes. Universal policies can transfer these assets tax-efficiently, preserving estate value and giving heirs options rather than obligations.

Pro Tip: If you currently hold low-yield bonds or CDs in a taxable account, ask your financial advisor whether repositioning some of that capital into a permanent life insurance policy would improve your after-tax return profile. The math often surprises people.

The risks are real and worth naming. Permanent policies cost more than term. If you underfund a policy or take excessive loans, it can lapse, triggering a tax bill on accumulated gains. Policy management requires attention. But for families focused on financial planning with life insurance as a long-term wealth tool, the tradeoffs are frequently favorable.

Annuity maximization: a powerful repositioning strategy

One of the most underused asset maximizing strategies involves deferred annuities. Many people hold annuities that have grown significantly over the years. The problem is that when those funds are distributed, they’re taxed as ordinary income, which can erode a substantial portion of the value.

Annuity maximization offers a structured solution. Here’s how it works:

-

You convert your deferred annuity into a Single Premium Immediate Annuity (SPIA), which begins paying income right away.

-

That income stream, after taxes, funds premiums on a permanent life insurance policy.

-

The death benefit from that policy passes to your heirs income-tax-free, often exceeding what they would have received from the annuity directly.

Consider a concrete example. A deferred annuity converted to a SPIA paid $11,026 annually. After taxes, the net income was $8,379. That amount funded a whole life policy with a $167,281 death benefit, turning a $100,000 annuity into a significantly larger inheritance.

| Starting asset | Annual SPIA income | After-tax income | Resulting death benefit |

|---|---|---|---|

| $100,000 deferred annuity | $11,026 | $8,379 | $167,281 |

Exchanging annuities for SPIAs that fund life insurance transforms taxable income into a tax-free wealth transfer. For retirees who don’t need the annuity income for living expenses, this strategy can substantially increase what they leave behind without requiring additional out-of-pocket investment.

The tax implications require careful planning. A 1035 exchange allows you to transfer funds between certain insurance products without triggering immediate taxes, but the rules are specific. Work with a tax-aware financial professional before executing this kind of repositioning.

Why timing and policy management matter

Here’s a truth that most people learn too late: delaying life insurance planning is not a neutral decision. Every year you wait, premiums rise and underwriting becomes more complex. For individuals between 50 and 65, this window is especially critical. The policies you can qualify for today may not be available in five years.

Active policy management is equally important once a policy is in place. A policy that isn’t reviewed regularly can drift off course. Here’s what ongoing management looks like in practice:

-

Monitor cash value growth against your original projections to catch underfunding early

-

Manage policy loans carefully because unpaid loans reduce your death benefit and can cause a policy to lapse

-

Review living benefits riders that allow you to access a portion of your death benefit if you’re diagnosed with a chronic or terminal illness

-

Reassess coverage levels as your estate grows, your family changes, or your financial goals shift

-

Explore life settlements before surrendering a policy you no longer want or need

That last point deserves emphasis. Secondary market sales may yield up to 8 times the insurance company’s surrender value. If you’re considering lapsing or surrendering a policy, you may be leaving a significant amount of money on the table. A life settlement, where you sell your policy to a third-party buyer, is a legitimate and often far more lucrative alternative.

Pro Tip: Integrate living benefits riders when you first purchase a policy rather than adding them later. They’re almost always cheaper at the point of sale, and they dramatically expand what your policy can do for you while you’re still alive.

Early underwriting preserves future optionality in estate planning, enabling life insurance to manage tax liabilities without forcing asset sales. The families who benefit most from life insurance asset maximization are those who start early and stay engaged throughout the policy’s life.

Practical steps for applying asset maximization

If you’re ready to move from understanding to action, start with what you already have. Many families own policies they haven’t reviewed in years. Here’s a straightforward process for getting started:

-

Audit your current policies. Identify whether you hold term or permanent coverage, and if permanent, what your current cash value is. Your annual policy statement contains this information.

-

Work with a financial professional. A fee-based advisor or insurance specialist can model different scenarios, including repositioning strategies, living benefits integration, and estate planning coordination.

-

Explore life settlements if you have an unwanted policy. Before you surrender or lapse, get a secondary market valuation to understand what your policy might be worth to a third-party buyer.

-

Coordinate with your estate plan. Life insurance owned inside an irrevocable life insurance trust (ILIT) can pass outside your taxable estate entirely, multiplying the efficiency of the strategy.

-

Schedule annual reviews. Your financial situation changes. Your policy strategy should keep pace. A yearly check-in with your advisor keeps the asset working as intended.

Life settlements for seniors and their advisors represent one of the most overlooked opportunities in personal finance. A policy that no longer fits your needs isn’t a sunk cost. It’s an asset with a market value that may surprise you.

My take on what most families get wrong

I’ve spent years watching families treat life insurance as a line item rather than a lever. They pay the premium, file the policy, and forget about it until someone dies. That approach leaves real money behind.

What I’ve found is that the families who benefit most from these strategies aren’t necessarily the wealthiest. They’re the most engaged. They ask questions. They review their policies. They work with advisors who see the full picture, not just the death benefit column.

The shift happening right now in 2026 is meaningful. Industry experts highlight a shift from death benefit focus to living benefits, using policies for income replacement and chronic illness care. That’s not a niche strategy anymore. It’s becoming standard practice for families who want their insurance to do more than collect dust.

The secondary market is another area where I see consistent missed opportunities. Advisors have a responsibility to discuss life settlements as an alternative to lapsing, yet many clients never hear about this option. A policy that feels like a burden could be worth hundreds of thousands of dollars to the right buyer.

My pragmatic advice: treat your life insurance policy the way you treat your investment portfolio. Review it. Optimize it. And when your needs change, explore every option before walking away from value you’ve already built.

— Scott Thomas

Unlock the full value of your life insurance policy

If this article has made you wonder whether your current policy is working as hard as it could, that’s a good instinct to follow. Many policyholders discover that they’re sitting on significantly more value than they realized, especially those with older permanent policies they no longer need.

Asset Life Settlements specializes in helping individuals and families turn life insurance policies into real financial assets through the life settlement process. Whether you’re exploring your options for the first time or ready to act, the team at Asset Life Settlements provides transparent, expert guidance from policy evaluation through final settlement. Learn more about how the process works or connect with an expert at Asset Life Settlements to find out what your policy may be worth today.

FAQ

What is life insurance asset maximization?

Life insurance asset maximization is the strategy of using permanent life insurance as a growing financial asset rather than just a death benefit, leveraging cash value accumulation, tax advantages, and wealth transfer features to improve overall financial outcomes.

How does cash value in a life insurance policy work?

Cash value grows tax-deferred inside a permanent life insurance policy and can be accessed through loans or withdrawals during your lifetime, though unpaid loans reduce the death benefit and withdrawals above your cost basis may trigger taxes.

What is annuity maximization in life insurance planning?

Annuity maximization converts a deferred annuity into a SPIA that generates income, which then funds a permanent life insurance policy, often resulting in a larger, tax-free inheritance for heirs than the original annuity would have provided.

Is it better to surrender a life insurance policy or sell it?

Selling a policy through a life settlement on the secondary market typically yields significantly more than surrendering it to the insurer. Secondary market sales can return up to 8 times the surrender value, making it worth exploring before lapsing any policy.

When should I start planning for life insurance asset maximization?

The earlier the better. Delays increase premiums and complicate underwriting, particularly for individuals between 50 and 65. Starting early preserves both affordability and the flexibility to integrate living benefits and estate planning strategies effectively.