Many people assume that converting a life insurance policy into cash is as simple as calling the insurer and cashing out. The reality is more nuanced. A viatical settlement is a legal financial transaction with real complexity, meaningful tax considerations, and long-term consequences for your estate and beneficiaries. If you or someone you care for is living with a terminal or chronic illness, understanding how this process works could mean the difference between leaving significant value on the table and accessing funds that genuinely change your quality of life.

Table of Contents

Key takeaways

| Point | Details |

|---|---|

| Viatical settlements convert policies to cash | Terminally or chronically ill policyholders can sell their life insurance for an immediate lump sum. |

| Payout is tied to life expectancy | The shorter the estimated life expectancy, the higher the percentage of face value you typically receive. |

| Federal tax exemption often applies | Proceeds for terminally ill sellers are generally tax-free under IRC 101(g), though chronic illness cases have additional rules. |

| Multiple offers matter | Getting competing bids through a licensed broker typically produces significantly better outcomes than accepting a single offer. |

| Loss of death benefit is permanent | Once ownership transfers, your beneficiaries no longer receive the death benefit from that policy. |

What is a viatical settlement and how does it work?

A viatical settlement is the sale of an in-force life insurance policy by a terminally or chronically ill policyholder. The buyer, called a viatical settlement provider, pays a lump sum that is less than the policy’s face value but more than its cash surrender value. In exchange, the buyer assumes all future premium payments and collects the full death benefit when the insured passes.

Three parties make this transaction work. The viator is the policyholder who sells. The provider is the institutional buyer. The broker represents the viator, shops the policy to multiple providers, and works to secure the best offer. Working with a qualified broker rather than going directly to a single provider is one of the most consequential decisions you can make in this process.

Here is how ownership shifts: once the sale closes, the buyer becomes the new policy owner and beneficiary. Your original beneficiaries receive nothing from this policy at death. That transfer is permanent and complete.

Pricing depends heavily on estimated life expectancy. Buyers model their return based on how long they expect to continue paying premiums before collecting the death benefit. Shorter life expectancy means a higher offer to you, because the buyer expects a faster return. This is also why investor return is inherently uncertain. If the insured outlives the projection, the buyer’s returns shrink.

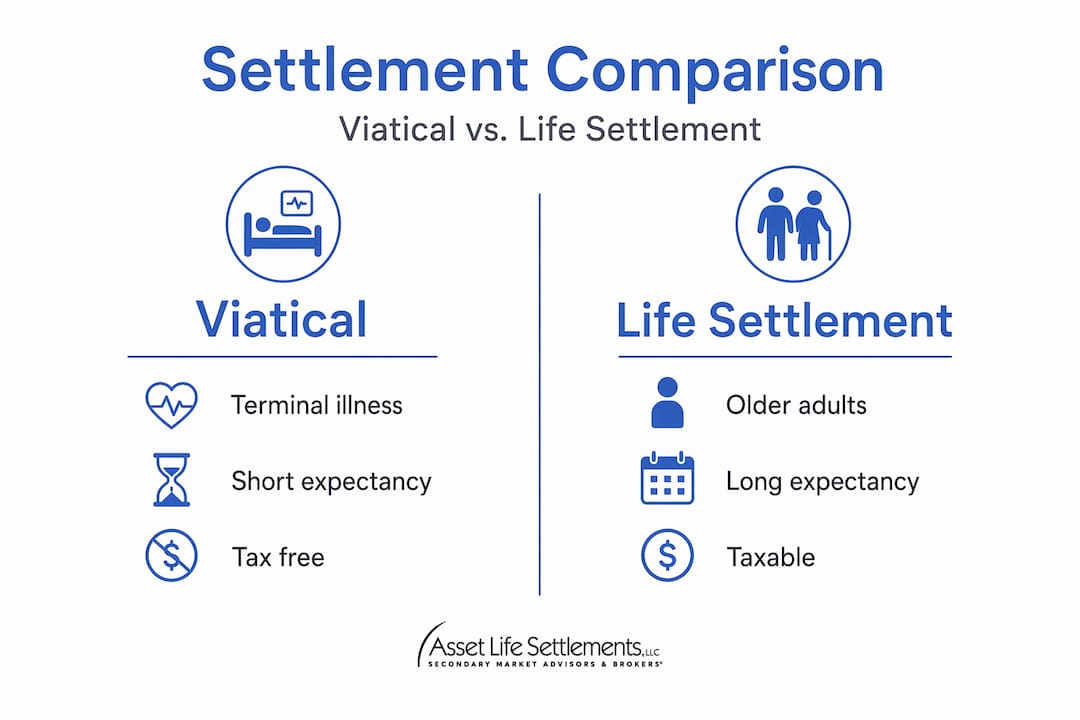

It is worth distinguishing a viatical settlement from two related options. A life settlement involves older adults who are not necessarily terminally ill, typically with a life expectancy above two years. An accelerated death benefit rider lets you access a portion of your death benefit directly from the insurer without selling the policy. Each has different trade-offs in terms of payout size, tax treatment, and ownership implications.

Pro Tip: Ask your insurer whether your policy includes an accelerated death benefit rider before pursuing a viatical settlement. If it does, compare both options side by side before committing to either.

Eligibility, valuation, and minimum payout rules

Not every policyholder qualifies for a viatical settlement. The process has specific eligibility requirements that filter both the person and the policy.

To qualify personally, you generally must have a terminal illness with a life expectancy of two years or less, or a chronic illness that meets IRS definitions. Some states extend eligibility to conditions that significantly impair daily living activities. The illness must be diagnosed and documented by a licensed physician.

On the policy side, eligible types typically include whole life, universal life, variable universal life, and convertible term policies with enough face value to make the transaction worthwhile. Most providers look for policies with a face value of at least $100,000. The policy also must have passed its two-year contestability period, during which the insurer could dispute claims based on application misrepresentations.

Once you apply, a medical underwriting firm reviews your records to estimate your life expectancy. That estimate is the single most important variable in calculating your offer. The viatical settlement process involves submitting medical release authorizations so underwriters can access your health history, physician notes, and specialist reports.

Valuation also accounts for the policy’s face value, projected future premiums the buyer will need to pay, and the return rate the buyer targets. A higher face value and shorter life expectancy generally result in a larger cash offer to you. A typical payout lands between 50% and 80% of the policy’s face value.

Consumer protection regulations set minimum payout floors. The National Association of Insurance Commissioners model regulations specify these thresholds:

| Life expectancy | Minimum payout (% of face value) |

|---|---|

| Less than 6 months | 80% |

| 6 to 12 months | 70% |

| 12 to 18 months | 65% |

| 18 to 24 months | 60% |

| More than 24 months | Case-by-case, state-specific |

These NAIC minimum payout floors represent the legal floor, not the expected outcome. Competitive bidding through an experienced broker often produces offers well above these minimums.

Pro Tip: Use a life settlement calculator to get a rough estimate of your policy’s value before entering any formal application. It frames expectations and helps you evaluate offers more clearly.

Tax implications and other financial considerations

The federal tax treatment of viatical settlement proceeds is one of the most important factors in evaluating this option. Under IRC 101(g), proceeds received by a terminally ill seller are generally tax-free at the federal level. That is a meaningful benefit compared to many other forms of asset liquidation.

Chronically ill sellers face a more complicated picture. Proceeds may still qualify for tax-free treatment, but only if the funds are used for costs related to the qualifying illness. The documentation requirements are more involved, and the rules have changed over time. Consulting a tax advisor before you close any transaction is not optional. It is a necessary step.

Beyond federal taxes, consider these additional financial implications:

-

Means-tested benefit programs. A lump-sum payment from a viatical settlement can affect your eligibility for Medicaid and Supplemental Security Income. Both programs apply asset and income tests. A sudden cash infusion could temporarily disqualify you until those funds are spent down.

-

Creditor claims. In some states, proceeds from life insurance policies enjoy creditor protection. Once the policy is sold and converted to cash, that protection may no longer apply. If you have outstanding debts or legal judgments, this distinction matters.

-

Spousal consent. Many states require a spouse’s written consent before a viatical settlement can close. This is particularly relevant for community property states where the policy may be considered a shared asset.

-

Loss of death benefit. This is the trade-off that surprises people most. When you sell, your beneficiaries receive nothing from that policy. That affects estate planning, dependent support, and any financial obligations you were expecting the policy to cover.

Comparing a viatical settlement to an accelerated death benefit rider requires looking beyond payout amounts. Sellers lose full ownership and beneficiary rights in a viatical settlement, while using an accelerated death benefit rider preserves ownership and only reduces the remaining death benefit proportionally. If preserving something for your heirs matters to you, the rider may be preferable even if the payout is smaller.

Practical steps for pursuing a viatical settlement

Knowing the mechanics of a viatical settlement is one thing. Knowing how to pursue one without making costly mistakes is another. Follow these steps to move through the process with confidence.

-

Gather your policy documents. Collect your current policy, any rider details, the most recent premium notices, and your insurer’s contact information. Providers will need all of this during underwriting.

-

Request medical records from your physicians. You will sign a medical release authorization that allows underwriters to access your health history directly. Having records organized in advance speeds up the timeline considerably.

-

Work with a licensed broker. A broker who represents your interests, not the buyer’s, is how you access competitive offers. Ask directly whether the broker has a fiduciary duty to you, and request a written agreement before sharing sensitive information.

-

Get multiple offers. Never accept the first offer without shopping the policy to multiple providers. The difference between the lowest and highest offer can be tens of thousands of dollars. Raising settlement options before surrendering or lapsing a policy can substantially increase your outcome.

-

Review the viatical contract terms carefully. Before signing, confirm the purchase price, the premium payment obligations post-sale, and what happens if there are disputes. Have an attorney review the contract independently.

-

Confirm escrow and ownership transfer procedures. Funds should be held in neutral escrow until the insurer officially confirms the ownership transfer. Releasing funds prematurely can lead to contract disputes that are difficult and costly to unwind.

-

Notify relevant advisors. Your financial planner, estate attorney, and accountant should all know about the transaction. The tax and estate planning implications touch every area of your financial life.

Pro Tip: Before finalizing, ask the broker how many providers will see your policy and how many bids you can expect. A broker who places your policy with only one or two providers is not working the competitive marketplace on your behalf.

My perspective on what clients get wrong

I have seen too many people surrender a life insurance policy for its cash value without ever asking whether a viatical settlement was an option. The insurer will not raise it. The policyholder assumes the surrender value is the best they can do. That assumption costs real money.

In my experience, the clients who benefit most from this process are the ones who bring their full financial picture to the table before making any moves. They ask about tax consequences. They think about what the death benefit was supposed to accomplish for their family. They are not in a rush to close the fastest deal. They are focused on the best deal.

The hardest conversations I have had are with people who surrendered policies weeks before consulting an advisor. A viatical settlement payout can be dramatically higher than the surrender value, but once the policy is gone, the opportunity is gone with it.

Fiduciary advisors often overlook settlements entirely because viatical settlements are not a standard topic in most financial planning curricula. That is changing, but slowly. If your advisor has not mentioned this option and you have a terminal or chronic illness, ask directly. Push the conversation. It is your asset.

The other thing I see undervalued is the escrow protection step. Most sellers focus on the payout number and barely glance at the closing mechanics. But escrow and insurer confirmation are your legal safeguards. They protect you from scenarios where funds are released before the transfer is confirmed, which leaves you in a vulnerable position with no policy and no certainty about your money.

— Jeff Hallman

How Asset Life Settlements can help you

When the stakes are this high, having an experienced advocate makes a real difference.

Asset Life Settlements works as a licensed broker representing your interests throughout the entire viatical settlement process. From policy evaluation to competitive bidding to closing, the team at Asset Life Settlements is focused on one outcome: securing you the highest possible value for your policy. Their track record speaks for itself. They secured a full $2 million settlement for an 85-year-old client when market conditions made that result look nearly impossible.

If you have a life insurance policy and you or a family member is living with a terminal or chronic illness, explore your viatical settlement options with Asset Life Settlements before making any decisions. The consultation is the starting point. What you learn there could change what you do next.

FAQ

What is a viatical settlement?

A viatical settlement is the sale of a life insurance policy by a terminally or chronically ill policyholder to a third-party buyer for a lump-sum cash payment. The buyer assumes premium payments and collects the death benefit when the insured passes.

How much cash can I get from a viatical settlement?

Payouts typically range from 50% to 80% of the policy’s face value, depending primarily on estimated life expectancy, the policy’s face amount, and future premium costs. NAIC model regulations set minimum floors to protect sellers.

Are viatical settlement proceeds taxable?

Proceeds for terminally ill sellers are generally tax-free at the federal level under IRC 101(g). Chronically ill sellers face additional documentation requirements, and proceeds must typically be applied to qualifying illness expenses to maintain that tax-free status.

How is a viatical settlement different from a life settlement?

Viatical settlements apply to terminally or chronically ill policyholders, typically with a life expectancy of two years or less. Life settlements generally involve older adults who are not terminally ill and have a longer life expectancy. The distinction also affects tax treatment and typical payout percentages.

How long does the viatical settlement process take?

The timeline varies based on how quickly medical records are gathered and how long underwriting takes, but most transactions close within 30 to 90 days after the application is submitted and all documentation is received.