Most people holding a life insurance policy have no idea what it’s actually worth on the open market. That gap in awareness is costly. Using our life settlement calculator gives you a concrete starting point for understanding your policy’s real market value before you make any decisions about lapsing, surrendering, or selling. Seniors who sold policies in 2024 received more than 6.5 times the carrier’s cash surrender value on average. That’s not a rounding error. That’s a fundamentally different financial outcome, and a good calculator is where it starts.

Table of Contents

-

Using our life settlement calculator: what it does and what it needs

-

What I’ve learned about calculators and realistic expectations

Key takeaways

| Point | Details |

|---|---|

| Calculators need quality inputs | Accurate estimates depend on age, health, policy type, face amount, premiums, and outstanding loans. |

| Premium modeling drives accuracy | Tools that don’t model policy charges and premium increases produce wide, unreliable value ranges. |

| Medical records aren’t required upfront | A well-designed calculator uses structured health questions to estimate life expectancy without initial uploads. |

| Sellers often leave money on the table | About 86% of seniors don’t know they can sell a policy instead of letting it lapse. |

| Calculator results are a starting point | Use outputs to compare your options and decide whether to pursue formal bids from qualified buyers. |

Using our life settlement calculator: what it does and what it needs

A life settlement calculator is not a magic number generator. It’s a modeling tool that takes specific inputs about your policy and your health, then applies mortality assumptions and premium projections to estimate what a buyer might pay for your policy today.

Professional-grade calculators are built around four pillars: eligibility screening, health underwriting to estimate mortality, understanding policy mechanics, and realistic premium optimization. Each pillar depends on the quality of information you provide.

Basic inputs every calculator needs:

-

Insured’s age and general health status

-

Policy type (term, universal life, whole life, variable)

-

Face amount (the death benefit)

-

Current annual or monthly premium

-

Whether the policy is still in force

Enhanced inputs that sharpen the estimate:

-

Insurance carrier and policy issue age

-

In-force illustration showing projected premium charges over time

-

Current cash value

-

Outstanding policy loans and whether they are growing or fixed

That last item matters more than most people expect. Outstanding loans reduce the net death benefit and increase lapse risk, both of which make a policy less attractive to buyers and lower the price they’re willing to pay. Including loan details in your estimate is not optional if you want accuracy.

Pro Tip: Request an in-force illustration from your insurance carrier before you start. This single document gives the calculator the premium projection data it needs to model costs accurately, which directly affects your estimated payout.

Premium obligations are typically the largest driver of policy value because they represent the ongoing cost a buyer must carry after purchasing your policy. A calculator that ignores realistic premium modeling is essentially guessing.

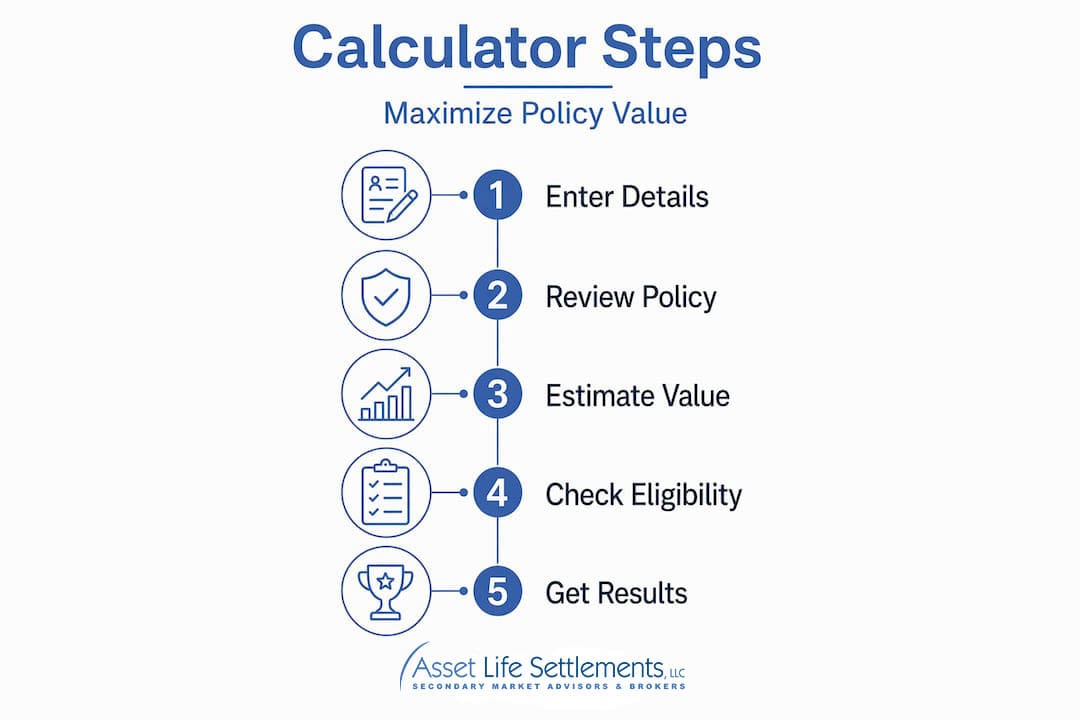

How to use the life settlement calculator step by step

You don’t need to have every document ready to get started. A good calculator is designed to give you directional value quickly, then refine that estimate as you add more detail.

-

Start with a basic estimate. Enter your age, general health category, policy type, face amount, and current premium. This gives you a broad range that tells you whether your policy is likely worth pursuing further.

-

Answer the health questionnaire honestly. A well-designed health questionnaire produces a reliable life expectancy range without requiring you to upload medical records upfront. Formal records are typically only requested if you decide to pursue actual bids. Answer based on diagnosed conditions, not how you feel generally.

-

Add your carrier and issue age. Different carriers have different policy structures. Knowing the carrier and how old the policy is helps the calculator apply the right product assumptions.

-

Input cash value and any outstanding loans. Even approximate figures here improve the estimate meaningfully. If you have a policy statement, use those numbers directly.

-

Upload or reference an in-force illustration if available. Using in-force illustration data yields the most accurate premium modeling, which is the single biggest variable in a realistic valuation. If you don’t have one, the calculator will use assumptions, and your range will be wider.

-

Review the output range and compare your options. The result is not a guaranteed offer. It’s an informed estimate of what the secondary market might pay, which you can compare against your policy’s cash surrender value or the cost of keeping coverage.

One misconception worth addressing directly: many people assume they need to hand over medical records before they can get any estimate. That’s not how a quality life settlement value estimator works. The health questionnaire approach is specifically designed to protect your privacy while still producing a meaningful estimate.

Pro Tip: If you want a tighter estimate rather than a wide range, prioritize getting the in-force illustration and your exact loan balance. Those two inputs have the biggest impact on narrowing the output.

Check the life settlement eligibility requirements before you spend time gathering documents. Knowing whether your policy and health profile qualify saves you significant effort.

Not all calculators are built the same

This is where a lot of people get misled. There is a wide spectrum of tools marketed as life settlement calculators, and the difference between a basic tool and a professional-grade one is significant.

| Feature | Basic calculator | Professional-grade calculator |

|---|---|---|

| Health assessment | Simple age/health category | Structured medical questionnaire with condition weighting |

| Premium modeling | Flat premium assumption | Actual policy charges modeled from in-force illustrations |

| Loan handling | Not included | Loan balance and growth rate factored into net benefit |

| Output precision | Wide range with broad disclaimers | Tighter estimate with underwriting-based mortality assumptions |

| Viatical vs. life settlement | Not differentiated | Separate modeling for terminal/chronic illness cases |

Calculators that don’t model policy charges, premium increases, or product design often produce imprecise, broad value ranges as a way of disclaiming their own limitations. If a tool tells you your policy is worth “between $50,000 and $400,000,” that range is not useful for decision-making.

Viatical calculators operate differently from standard life settlement tools. Viatical cases reflect shorter life expectancy and compressed premium periods, which changes the valuation math significantly. If you or your insured has a terminal or chronic illness, a standard life settlement calculator will undervalue the policy because it’s not built for that mortality profile.

Be cautious of tools that are primarily designed to capture your contact information rather than deliver a real estimate. The best life settlement calculators are transparent about their methodology and give you a result you can actually use.

Practical ways to maximize your life settlement value

Getting a number from a calculator is step one. Using that number well is where most people need guidance.

-

Gather precise documents before going formal. The more accurate your inputs, the stronger your position when actual buyers review your policy. Vague or estimated figures create gaps that buyers use to justify lower offers.

-

Compare your options side by side. Your calculator output should be weighed against the policy’s cash surrender value and the cost of maintaining coverage. Seniors who sold their policies received dramatically more than the surrender value in most cases, but that comparison only becomes clear when you have both numbers in front of you.

-

Understand what drives your estimate up or down. Premium obligations are the biggest cost a buyer assumes. If your policy has high ongoing premiums, that reduces buyer interest and lowers offers. Knowing this lets you have a more informed conversation with a broker.

-

Use the estimate to decide whether to engage a broker. If the calculator output is significantly above your surrender value, that’s a signal worth acting on. A qualified broker can take your estimate to a competitive marketplace where multiple buyers bid, which is how you actually maximize the final payout.

-

Don’t treat the calculator output as a final offer. It’s a life settlement estimation tool, not a binding quote. Real offers depend on formal underwriting, full policy review, and market conditions at the time of sale.

The life settlement process moves from estimate to formal evaluation to competitive bidding. Your calculator result is the foundation that determines whether the rest of that process is worth pursuing.

There were 2,699 life settlement transactions in 2024 totaling $601 million in face value. That secondary market is active and competitive. Your policy may have a place in it.

What I’ve learned about calculators and realistic expectations

I’ve worked with enough policyholders to know that the biggest problem isn’t a lack of tools. It’s misplaced trust in the wrong ones.

I’ve seen people walk away from significant value because a basic calculator gave them a low estimate and they assumed that was the market. What they didn’t know was that the tool they used had no premium modeling, no health underwriting, and no way to account for their specific policy structure. It was producing a number, but not a defensible one.

The calculators that actually serve sellers well are the ones built the way real buyers think. Buyers care about how long they’ll be paying premiums, what those premiums will cost over time, and what the net death benefit looks like after loans. A calculator that skips those variables isn’t modeling a life settlement. It’s modeling a rough guess.

My honest advice: use the calculator as a first step, not a final answer. If the output surprises you in either direction, dig deeper. Get the in-force illustration. Talk to a broker who will advocate for your interests. The estimate is a starting point for a conversation, not the end of one.

I’ve also seen the other side of this. When a policyholder comes in with detailed documentation, a clear understanding of their policy’s premium trajectory, and a realistic sense of value from a good calculator, the process moves faster and the outcomes are better. Preparation is leverage.

— Jeff Hallman

Get a real valuation with Asset Life Settlements

Using a life settlement calculator is the right first move. The next move is working with a broker who can take that estimate and turn it into a competitive offer from qualified buyers.

Asset Life Settlements works as a fiduciary broker, meaning we represent your interests, not the buyer’s. We bring your policy to a competitive marketplace where multiple institutional buyers bid, which is how policyholders consistently receive offers well above what any single buyer would propose. Our broker advantage is built on transparency, experience, and a track record of securing full value even in difficult circumstances.

There’s no cost and no obligation to get a formal evaluation. If your calculator results suggest your policy has real market value, we can help you find out exactly what that value is. Explore the full life settlement process to understand what happens after your estimate, and reach out to our team when you’re ready to take the next step.

FAQ

What inputs does a life settlement calculator need?

A basic life settlement calculator needs the insured’s age, health status, policy type, face amount, and current premium. Adding carrier details, cash value, outstanding loans, and an in-force illustration produces a significantly more accurate estimate.

Do I need to upload medical records to use a calculator?

No. A well-designed life settlement value estimator uses a structured health questionnaire to estimate life expectancy without requiring medical records upfront. Records are typically only requested if you decide to pursue formal bids.

Why do some calculators give such wide value ranges?

Wide ranges usually indicate the tool lacks premium modeling and health underwriting depth. Calculators without policy charge modeling use broad disclaimers to cover their imprecision, which limits their usefulness for real decisions.

How does a life settlement differ from surrendering a policy?

Surrendering a policy returns only the cash value set by the carrier. A life settlement sells the policy to a third-party buyer on the secondary market, where competitive bidding typically produces a much higher payout than the surrender value.

When should I contact a broker after using the calculator?

If your life settlement payout calculator estimate is meaningfully higher than your policy’s cash surrender value, that’s a strong signal to engage a qualified broker. A broker can bring your policy to multiple buyers and negotiate on your behalf to maximize the final offer.