Most financial professionals understand that a life settlement involves selling a life insurance policy for more than its cash surrender value. What far fewer recognize is that the role of medical underwriting in life settlement transactions is what ultimately determines how much a client walks away with. This is not simply a health status review. It is a detailed actuarial process that shapes every offer on the table, and misunderstanding it costs policyholders real money. Here is what you need to know to protect your clients and advocate for their best financial outcome.

Table of Contents

Key Takeaways

| Point | Details |

|---|---|

| Medical underwriting drives offer value | Life expectancy estimates from underwriters directly set the price investors will pay for a policy. |

| Incomplete health data hurts sellers | Missing or poorly formatted medical records can lower settlement offers significantly below fair market value. |

| AI is accelerating the process | Automated tools now handle up to 70% of cases, reducing review time and improving pricing accuracy. |

| Regulation creates advisor obligations | In 43 U.S. states, life settlements are regulated, with six states requiring carriers to notify policyholders of settlement options. |

| Brokers with underwriting expertise matter | Working with firms that prioritize thorough medical assessment produces more competitive and accurate offers for your clients. |

How medical underwriting works in life settlements

Medical underwriting in the life settlement context is a structured evaluation of a policyholder’s health history to generate a life expectancy estimate. That estimate becomes the foundation for every purchase offer made by institutional investors on the secondary market.

The process draws on several data sources:

-

Attending physician statements (APS): Detailed records from the client’s primary care doctor and specialists

-

Medical history questionnaires: Self-reported data on diagnoses, medications, surgeries, and lifestyle factors

-

Lab results and diagnostic imaging: Objective clinical markers that underwriters use to assess mortality risk

-

Prescription drug histories: Medication profiles that reveal chronic conditions or treatment status

-

Electronic health records (EHR): Digital clinical data that increasingly supplements or replaces paper records

Once this data is assembled, the underwriter applies it to actuarial mortality tables and generates a life expectancy estimate with a confidence interval. Mortality ratings and confidence intervals reflect both the expected lifespan and the statistical certainty around that estimate. A tighter confidence interval generally produces a more defensible offer.

Data quality matters enormously here. A client whose records arrive incomplete, in illegible scanned PDFs, or missing key specialist notes will receive a less accurate underwriting assessment. That inaccuracy rarely benefits the seller. When underwriters cannot fully assess risk, they price conservatively, meaning lower offers.

Pro Tip: Before submitting a client’s case for life settlement evaluation, gather and organize all medical records from the past five years, including specialist notes, lab work, and prescription histories. Thorough documentation is one of the most direct ways to support a stronger offer.

Medical underwriting’s impact on settlement value

The connection between underwriting findings and settlement payouts is direct and significant. Institutional investors buy life insurance policies expecting to pay future premiums and collect the death benefit. The shorter the estimated life expectancy, the higher the present value of that expected payout, and the more an investor will offer today.

Settlement payouts typically range from 10% to 25% of the face value of the policy, depending heavily on underwriting findings. On a $500,000 policy, that is a spread of $50,000 to $125,000. The difference between a thorough and a superficial medical assessment can easily determine where within that range your client lands.

This is also where life settlement underwriting diverges sharply from traditional life insurance underwriting. Consider the contrast:

| Factor | Traditional insurance underwriting | Life settlement underwriting |

|---|---|---|

| Goal | Assess insurability and premium risk | Estimate life expectancy to price a purchase offer |

| Preferred health profile | Healthier applicants get lower premiums | Shorter life expectancy increases policy value |

| Data used | Health history at policy application | Current and recent health records |

| Decision outcome | Accept, decline, or rate the policy | Generate a life expectancy and associated offer |

| Who benefits from detail | The insurer | The policyholder/seller |

The difference in incentive structure is critical. In a traditional insurance context, a client’s health problems work against them. In a life settlement, a more accurate picture of health, including serious but stable chronic conditions, can actually support a stronger offer. Conditions like cardiovascular disease, diabetes with complications, or certain cancers that have been treated carry real actuarial weight.

Pro Tip: Never assume a client is ineligible for a meaningful settlement based on a surface-level health review. Let the full underwriting process determine value before drawing conclusions.

Regulatory environment and fiduciary responsibilities

Life settlements do not operate in a regulatory vacuum. 43 U.S. states regulate life settlements, with specific requirements around licensing, disclosure, and market conduct. Six states, including Washington, Wisconsin, Oregon, Maine, Kentucky, and New Hampshire, require carriers to notify policyholders of their settlement options before a policy lapses.

That regulatory framework creates both a floor of consumer protection and a responsibility for financial advisors. Consider what this means for your practice:

-

Fiduciary duty extends to policy disposition. If you advise a client to lapse or surrender a policy without exploring its secondary market value, you may be failing your fiduciary obligation.

-

Disclosure is increasingly mandated. As more states adopt notification requirements, the expectation that advisors raise the settlement option becomes more formalized.

-

Missed conversations have real costs. Many valuable policies lapse or are surrendered because advisors never raised the settlement option, leaving clients with far less than their policy was worth.

-

FINRA guidance reinforces the conversation. Regulatory bodies have signaled that life settlement awareness is part of responsible client advising.

The importance of medical underwriting is embedded in this regulatory context. Without an accurate underwriting assessment, neither you nor your client can know whether a policy has meaningful secondary market value. Recommending a lapse or surrender before a settlement evaluation is completed is not a neutral act. It is a decision with financial consequences.

Technology transforming the underwriting process

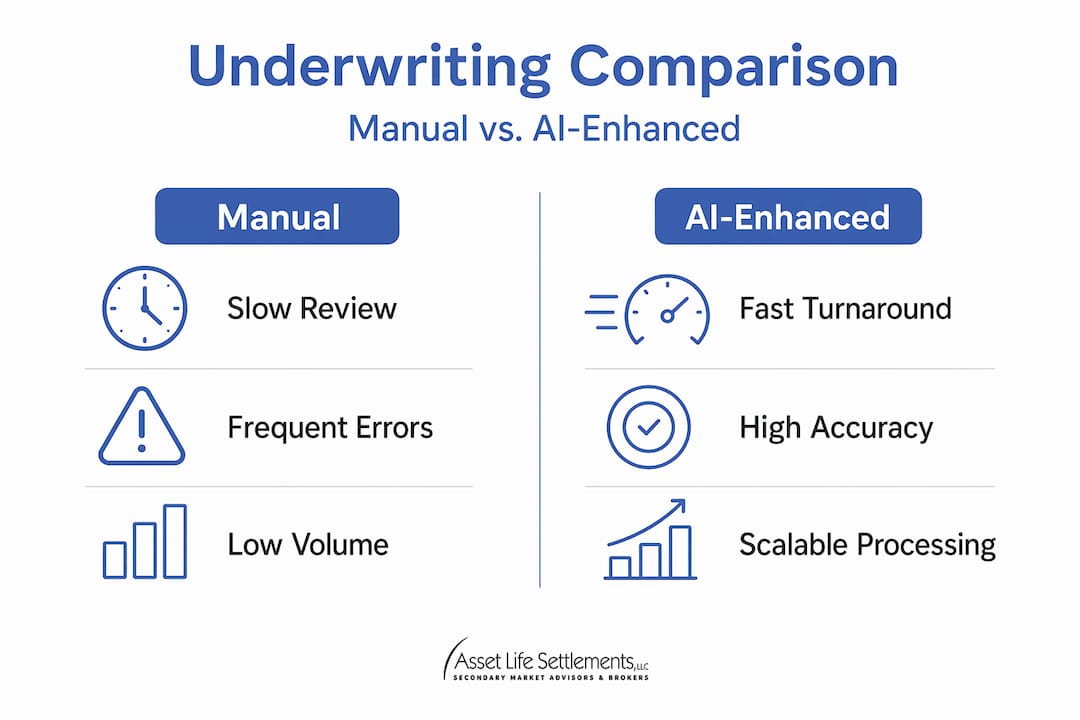

The life settlement underwriting process is changing rapidly, and the direction of change benefits both advisors and their clients. The shift from manual paper-based reviews to AI-assisted and digitally integrated assessments is accelerating.

Historically, underwriters reviewed medical records in human-readable PDF formats, a slow and error-prone process. Carriers increasingly push toward structured digital data formats that reduce manual errors and speed up processing. In parallel, AI tools now generate structured clinical summaries from raw medical records, flagging the conditions and indicators most relevant to mortality assessment.

The scale of adoption is notable. AI-based tools now process up to 70% of cases automatically at some high-volume life settlement operations, reducing the time underwriters spend on routine record review. One provider reports a user managing over 10,000 life settlement submissions annually who relies on AI summaries for the majority of that volume.

| Underwriting method | Speed | Accuracy | Volume capacity |

|---|---|---|---|

| Manual PDF review | Slow (days to weeks) | Dependent on reviewer experience | Low |

| Digitized EHR data | Fast (hours to 1 day) | High, with consistent formatting | Moderate to high |

| AI-assisted summary tools | Very fast (minutes to hours) | High, with structured outputs | Very high |

EHR release rates reached 52% in 2025, with 74% of those records delivered within one day. That speed directly reduces the time between policy submission and final offer, which benefits sellers who need timely decisions.

Pro Tip: When evaluating settlement brokers, ask specifically about their underwriting technology stack. Firms that integrate EHR data and AI-assisted review produce faster and more accurate assessments, which translates to better-informed offers for your clients.

Practical guidance for financial professionals

Integrating medical underwriting knowledge into your advisory practice is not about becoming a clinical expert. It is about knowing when to act, what to look for, and who to partner with.

Here is a practical framework for incorporating life settlement evaluations into your client work:

-

Screen eligible clients proactively. Senior clients over 65 with permanent life insurance policies, particularly those no longer affordable or needed, are the primary candidates. Review the eligibility criteria before assuming a policy does not qualify.

-

Initiate the medical record conversation early. The completeness of health documentation directly affects underwriting accuracy. Start gathering records before submitting for evaluation, not after.

-

Understand the life expectancy report. When you receive an underwriting summary, review the mortality rating and the confidence interval. A high confidence interval with a shorter life expectancy projection typically supports a stronger offer.

-

Avoid the surrender default. Premium financing arrangements and other complex insurance structures are frequently mishandled because advisors assume the insured’s death is the only exit. Settlement is often a better and more accessible option.

-

Partner with brokers who prioritize underwriting depth. A broker that submits cases to multiple institutional buyers and understands how to frame medical findings will consistently produce more competitive offers. Review how they approach the full settlement process before committing.

-

Document your disclosures. Once you have introduced the settlement option and reviewed underwriting findings with a client, document that conversation. Your fiduciary responsibilities require it, and your records protect both you and your client.

My perspective on underwriting literacy in life settlements

I have watched advisors lose significant settlement value for their clients, not because the policies were not valuable, but because no one took the time to understand what the medical underwriting was actually saying. The report sits on a desk, the advisor skims the life expectancy number, and the case gets submitted without context or advocacy.

In my experience, the biggest gap in this space is not regulatory or technological. It is interpretive. Advisors who know how to read a mortality rating, who understand the difference between a 12-month and 48-month life expectancy estimate, and who can communicate those findings clearly to a client are the ones generating the best outcomes. Everyone else is guessing.

I have also seen the AI shift change what is possible at scale. Faster underwriting does not just mean faster offers. It means more accurate pricing, more competitive bids, and stronger advocacy for your client’s financial interests. That is not a minor operational detail. It is a structural advantage for advisors who choose the right partners.

My honest advice: stop treating medical underwriting as a back-office function you hand off and forget. Learn enough to ask the right questions, push back when data seems incomplete, and insist on working with firms that treat underwriting accuracy as a priority. Your clients will notice the difference in their settlement offers.

— Jeff Hallman

Work with Asset Life Settlements for underwriting-backed results

Asset Life Settlements brings decades of experience to every case, with an underwriting-informed approach that maximizes offer accuracy and final settlement value. The team works directly with financial professionals to evaluate policies thoroughly, from initial medical record review through final offer negotiation, making sure no value is left on the table.

Whether your client holds a policy they can no longer afford or one that no longer serves their financial plan, Asset Life Settlements has the tools, expertise, and institutional relationships to get a fair and competitive result. The firm has secured a full $2 million for an 85-year-old client in a challenging market, demonstrating what rigorous underwriting and strong advocacy can achieve.

Connect with the professional resources at Asset Life Settlements, or explore the step-by-step life settlement process to see how the firm supports advisors at every stage.

FAQ

What is the role of medical underwriting in a life settlement?

Medical underwriting in a life settlement evaluates a policyholder’s health history to generate a life expectancy estimate, which directly determines the purchase price institutional investors will offer for the policy. The more thorough and accurate the assessment, the more defensible and competitive the resulting offer.

How does life expectancy affect settlement value?

A shorter life expectancy estimate increases the present value of the death benefit for buyers, which typically translates to a higher offer for the seller. Settlement payouts range from 10% to 25% of face value, and underwriting accuracy is a primary factor in where a specific case lands within that range.

Are financial advisors required to discuss life settlements with clients?

In 43 regulated states, life settlements are subject to specific legal requirements, and six states mandate carrier disclosure before policy lapse. Fiduciary advisors have an ethical obligation to raise the settlement option when a policy holds meaningful secondary market value.

How is AI changing life settlement underwriting?

AI tools now handle up to 70% of cases automatically at high-volume settlement operations, reducing review time from days to hours and producing more consistent mortality assessments. Faster, more accurate underwriting benefits sellers by supporting better-informed and more competitive offers.

What types of health conditions improve a life settlement offer?

Conditions that shorten life expectancy within actuarial models, such as advanced cardiovascular disease, treated cancers, or diabetes with documented complications, can support stronger settlement valuations. The key is accurate, complete documentation. An incomplete medical record can obscure conditions that would otherwise improve the offer.