A life settlement converts a life insurance policy into immediate cash by selling it to a third-party buyer, while a reverse mortgage converts home equity into a loan you never repay monthly while living in your home. These are the two most powerful retirement liquidity tools available to seniors today, and understanding the life settlement vs reverse mortgage explained comparison can mean the difference between leaving money on the table and funding a comfortable retirement. Both options let you access value locked in assets you already own, without selling your home outright or surrendering a policy for pennies. The right choice depends entirely on what assets you hold, what obligations you can manage, and what your heirs need.

How does a reverse mortgage work and what are its requirements?

A federally insured reverse mortgage known as a Home Equity Conversion Mortgage (HECM) allows homeowners age 62 and older to borrow against their home equity without making monthly principal or interest payments. The loan becomes due only when you move out permanently, sell the home, or pass away. This structure makes it attractive for seniors who are house-rich but cash-limited.

To qualify, you must own your home outright or carry a small remaining mortgage balance, and the home must be your primary residence. You will also need to complete a HUD-approved counseling session before closing. The HECM program is administered by the Federal Housing Administration (FHA), which sets loan limits and insurance requirements.

Once approved, you can receive funds in several ways:

-

Lump sum: A single upfront payment, typically at a fixed interest rate

-

Line of credit: Draw funds as needed, with the unused portion growing over time

-

Monthly payments: Fixed disbursements for a set term or for as long as you live in the home

-

Combination: Mix a line of credit with monthly payments

The non-recourse feature is one of the most misunderstood protections in the program. Heirs never owe more than the home’s appraised value at the time of repayment, even if the loan balance has grown beyond that amount. They can sell the home to repay the loan, refinance it to keep the property, or walk away without further liability.

However, no monthly mortgage payment does not mean no obligations. You must continue paying property taxes, homeowner’s insurance, HOA dues, and maintain the home to avoid default. Missing even a single year of property tax or insurance payments can trigger the loan due status, which is a risk many borrowers underestimate.

Pro Tip: Set up automatic payments for property taxes and homeowner’s insurance the moment your reverse mortgage closes. Reverse mortgage default risk arises not from loan interest, but from failure to meet property charges, and automated reminders are your best defense.

Reverse mortgage costs include origination fees, closing costs, and FHA mortgage insurance premiums. The loan balance grows over time as interest and fees accumulate, which reduces the equity available to your heirs.

What is a life settlement and how does the process work?

A life settlement is defined as the sale of an existing life insurance policy to a third-party institutional buyer in exchange for a lump sum cash payment greater than the policy’s surrender value. The industry term is “life settlement,” and it applies specifically to permanent life insurance policies such as whole life, universal life, and variable universal life. Term policies are generally not eligible unless they are convertible.

Life settlement exploration costs nothing upfront since brokers are compensated from the settlement proceeds. This makes it a low-risk option to evaluate, even if you ultimately decide not to proceed. Seniors aged 70 and older with policies valued at $100,000 or more are the most common candidates, though eligibility depends on several factors:

-

Policy type: Permanent policies are preferred; convertible term policies may qualify

-

Face value: Policies under $100,000 are rarely competitive in the secondary market

-

Health status: Buyers use medical underwriting to assess life expectancy; a change in health since the policy was issued often increases the settlement offer

-

Premium burden: Policies with high ongoing premiums that the owner no longer wants to pay are strong candidates

Once you decide to explore a settlement, a broker like Asset Life Settlements submits your policy to multiple institutional buyers to create a competitive bidding environment. The highest offer is presented to you, and you decide whether to accept. The life settlement process typically takes 60 to 120 days from submission to funding.

When you sell your policy, the buyer takes over premium payments and eventually collects the death benefit. Your heirs lose the death benefit, but you gain immediate cash. Life settlements unlock funds from policies seniors no longer want or need, turning what would have been a surrendered or lapsed policy into real retirement capital.

Pro Tip: Before surrendering a policy back to the insurance company, always check life settlement eligibility first. Surrender values are almost always lower than what the secondary market will pay.

How do life settlements and reverse mortgages compare on costs, risks, and liquidity?

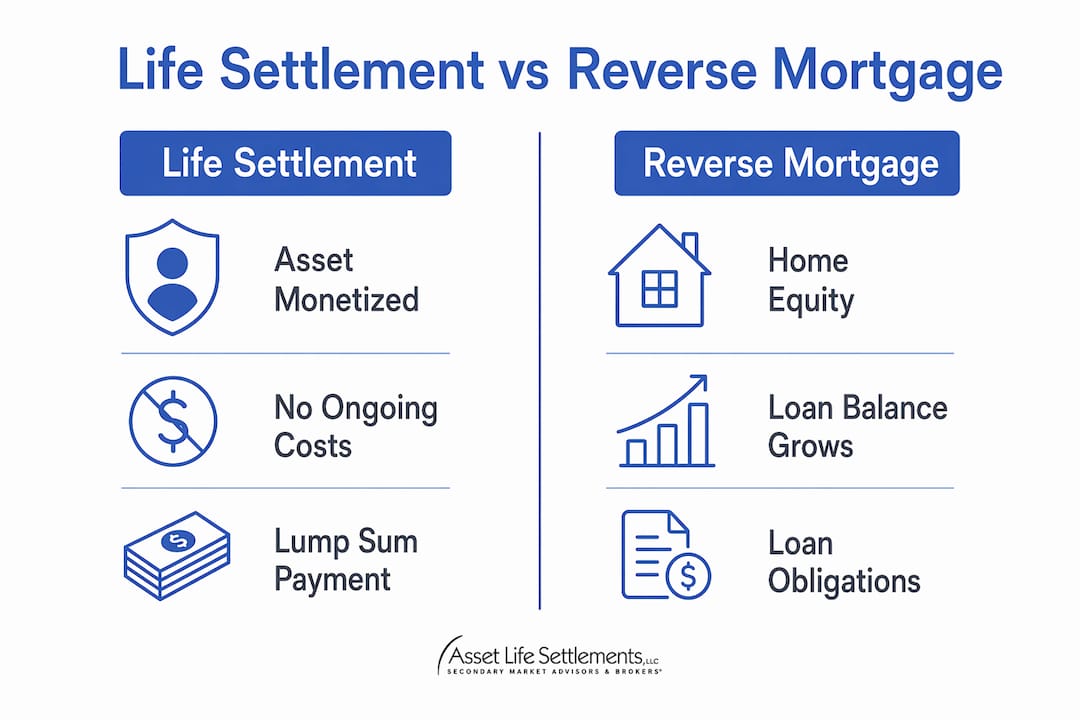

The life settlement vs reverse mortgage comparison comes down to which asset you want to monetize and what trade-offs you can accept. Here is a direct side-by-side breakdown:

| Feature | Life Settlement | Reverse Mortgage |

|---|---|---|

| Asset monetized | Life insurance policy | Home equity |

| Upfront cost | None (broker paid from proceeds) | Origination fees, closing costs, FHA insurance premiums |

| Ongoing obligations | None after settlement closes | Property taxes, insurance, HOA, home maintenance |

| Impact on heirs | Loss of death benefit | Reduced home equity; non-recourse protection applies |

| Cash delivery | Lump sum | Lump sum, line of credit, or monthly payments |

| Risk of losing asset | Policy ownership transfers to buyer | Home can be lost to foreclosure if obligations are missed |

| Loan balance growth | Not applicable | Balance grows over time due to interest and fees |

The reverse mortgage carries a hidden complexity that many seniors miss. Loan balances grow over time due to accruing interest and mortgage insurance premiums, which can significantly reduce the equity your estate retains. For heirs who expect to inherit the family home, this is a meaningful consideration.

A life settlement, by contrast, has no ongoing financial obligations after the transaction closes. You receive your cash, your premium payments stop, and the buyer manages the policy from that point forward. The trade-off is permanent: the death benefit is gone.

Liquidity timing also differs. A life settlement delivers a single lump sum, which is ideal for covering a large expense such as long-term care, debt payoff, or a major purchase. A reverse mortgage line of credit grows over time and can serve as a flexible safety net, making it better suited for ongoing income supplementation alongside Social Security or other retirement income.

When should you choose a life settlement vs a reverse mortgage?

Mapping each tool to specific financial goals clarifies the decision: use a reverse mortgage to access housing equity while retaining your home, and use a life settlement to monetize a life insurance policy you no longer need. Here is a practical framework for deciding:

-

Choose a reverse mortgage if you want to stay in your home long-term, need flexible ongoing income, and can reliably manage property taxes and insurance payments.

-

Choose a life settlement if you hold a permanent life insurance policy you no longer need, want to eliminate premium payments, and prefer a clean lump sum with no future obligations.

-

Consider both if you own a home with substantial equity and carry a permanent life insurance policy. Combining both options can diversify your retirement income sources and reduce dependence on any single asset.

-

Prioritize a life settlement if your health has declined since the policy was issued, because medical underwriting by buyers often results in higher offers for policyholders with reduced life expectancy.

-

Prioritize a reverse mortgage if your primary concern is housing security and you want to avoid any transaction that affects your estate’s real property.

Your housing plans matter enormously. If you intend to move to assisted living within five years, a reverse mortgage may not make sense because the loan becomes due when you leave the home. A life settlement, by contrast, has no residency requirement and closes regardless of your living situation.

Consulting a financial advisor who understands both products is the most reliable way to model outcomes. Many advisors do not routinely offer life settlements during policy reviews, which means the option is frequently overlooked. Asking your advisor directly about life settlement eligibility before any policy review concludes is a step worth taking.

Key takeaways

A life settlement delivers immediate cash from a life insurance policy with no ongoing obligations, while a reverse mortgage provides flexible home equity access that requires continued compliance with property charges to avoid default.

| Point | Details |

|---|---|

| Life settlement defined | Selling a permanent life insurance policy to a third-party buyer for a lump sum greater than its surrender value. |

| Reverse mortgage obligations | No monthly mortgage payment does not eliminate taxes, insurance, and maintenance requirements. |

| Cost comparison | Life settlements have no upfront cost; reverse mortgages carry origination fees, closing costs, and insurance premiums. |

| Heir impact | Life settlements eliminate the death benefit; reverse mortgages reduce home equity but carry non-recourse protection. |

| Best combined strategy | Seniors with both a home and a permanent policy can use both tools to diversify retirement income. |

Why most seniors are sitting on more retirement capital than they realize

After years of working with seniors on retirement liquidity decisions, I have found one pattern that repeats itself constantly: people know about reverse mortgages, but almost nobody walks in knowing they can sell their life insurance policy. That gap costs seniors real money.

The life settlement market is not new. Institutional buyers have been purchasing policies for decades. But because most financial advisors do not bring it up proactively, policyholders either surrender their policies for a fraction of their value or let them lapse entirely. Both outcomes leave cash on the table that rightfully belongs to the policyholder.

My honest view is that the reverse mortgage vs life settlement question is often framed as an either/or decision when it should be a both/and conversation. If you own a home and carry a permanent life insurance policy you no longer need, you have two separate assets that can each generate retirement income. Treating them independently, and evaluating each on its own merits, almost always produces better outcomes than defaulting to one product because it is more familiar.

The one caution I give consistently: do not enter a reverse mortgage without a clear plan for managing property taxes and insurance. I have seen seniors lose homes not because they ran out of equity, but because they missed a single year of tax payments. That risk is real and preventable.

Seek personalized advice from a professional who has experience with both products. The right combination depends on your health, your housing plans, your heirs’ expectations, and your income needs. No article, including this one, replaces that conversation.

— Scott Thomas

Explore your life settlement options with Asset Life Settlements

If you hold a permanent life insurance policy and want to know what it is worth on the secondary market, Asset Life Settlements makes the evaluation process straightforward and free.

Asset Life Settlements is a trusted life settlement broker with a proven track record of securing maximum value for policyholders. The firm recently secured the full $2 million face value for an 85-year-old client in a challenging market, demonstrating what competitive bidding can achieve. There are no upfront costs to explore eligibility, and you are never obligated to accept an offer. Start by reviewing the full settlement process to understand each step from policy evaluation to funding. When you are ready to find out what your policy could be worth, contact Asset Life Settlements for a no-obligation consultation.

FAQ

What is the main difference between a life settlement and a reverse mortgage?

A life settlement converts a life insurance policy into a lump sum by selling it to a third-party buyer, while a reverse mortgage converts home equity into a loan that is repaid when you leave the home. They monetize different assets and carry different obligations.

Who qualifies for a life settlement?

Seniors aged 70 and older with permanent life insurance policies valued at $100,000 or more are the strongest candidates. Health status and premium burden also factor into eligibility and the size of the offer.

Can you lose your home with a reverse mortgage?

Yes. Missing property tax or insurance payments for even a single year can trigger loan default and foreclosure, even if you owe nothing on the original loan balance.

Is it possible to use both a life settlement and a reverse mortgage?

Yes. Seniors who own a home and carry a permanent life insurance policy can use both tools to diversify retirement income, accessing housing equity through a reverse mortgage and converting an unneeded policy through a life settlement.

Does a life settlement affect Social Security or Medicare benefits?

A life settlement produces taxable income, which may affect means-tested benefits. Consulting a tax advisor or financial planner before completing a settlement is the right step to understand the full impact on your specific situation.