Every year, seniors and their advisors surrender or lapse life insurance policies without ever asking a critical question: could this policy be worth more sold than abandoned? When you include life settlement in a wealth transfer plan, you give clients access to a legitimate, regulated financial tool that can generate substantially more cash than the carrier’s surrender value. This guide walks through what qualifies, how the process works, and how to avoid the costly mistakes that have caused advisors and policyholders to leave significant money on the table.

Table of Contents

-

How to include life settlement in a wealth transfer plan: the prerequisites

-

Common mistakes when adding life settlements to wealth transfer strategies

-

What clients gain when life settlements are part of the plan

Key takeaways

| Point | Details |

|---|---|

| Life settlements beat surrender | Selling a qualifying policy on the secondary market typically yields more than the carrier’s cash surrender value. |

| Eligibility has clear criteria | Seniors aged 65 and older with permanent policies over $100,000 face value are the most common qualifying candidates. |

| Fiduciary duty is at stake | Advisors who skip the settlement evaluation before policy lapse risk both asset loss and a breach of fiduciary obligation. |

| Evaluation carries no downside | If no bids come in, the policy can be surrendered as originally planned, making the review a zero-risk step. |

| Proceeds open reinvestment doors | Settlement funds can be redirected into annuities, trusts, or other wealth transfer vehicles to strengthen the overall plan. |

How to include life settlement in a wealth transfer plan: the prerequisites

Before you can integrate a life settlement into any planning strategy, you need a clear picture of what a life settlement actually is and whether a given policy qualifies.

A life settlement is the sale of an existing life insurance policy to a third-party buyer for a lump sum that exceeds the cash surrender value but is less than the net death benefit. The buyer assumes premium payments and collects the death benefit when the insured passes. For the policyholder, it converts an underperforming or unwanted asset into immediate, usable capital.

Who and what qualifies

Life settlements typically target seniors with permanent policies carrying a face value over $100,000. The most relevant eligibility factors are:

-

Insured’s age: Generally 65 or older, though health impairments can make younger insureds eligible

-

Policy type: Universal life, whole life, and convertible term policies are the most common candidates

-

Face amount: Policies under $100,000 rarely attract competitive bids

-

Health status: Declining health often increases settlement value because it shortens the buyer’s expected premium-paying period

-

Premium affordability: Policies the owner can no longer afford or no longer needs are strong candidates

You can review the full eligibility requirements before initiating any client conversation.

The regulatory landscape

43 states regulate life settlement transactions, providing meaningful consumer protections around disclosure, broker licensing, and transaction timelines. Six of those states go further, legally requiring advisors to disclose the settlement option before a policy lapses or is surrendered. That is not a soft best practice. It is the law.

A common misconception is that life settlements are obscure or risky products. They are not. They operate within a structured secondary market, and broker fees are capped by statute, meaning the evaluation costs nothing out of pocket for the policyholder.

Pro Tip: Review your state’s specific disclosure requirements before any policy surrender conversation. In states with mandatory disclosure laws, skipping this step is not just a missed opportunity. It is a compliance failure.

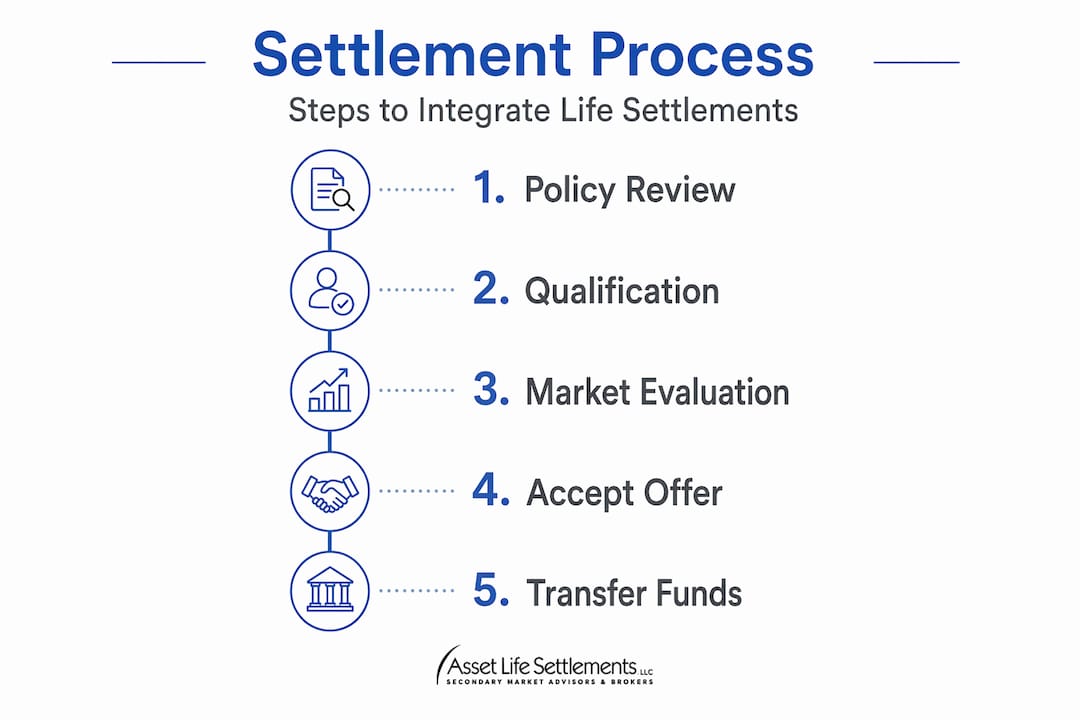

The step-by-step process for integrating life settlements

Once you’ve confirmed a policy may qualify, the path to incorporating it into a wealth transfer plan follows a clear sequence.

-

Identify and flag qualifying policies. During any policy review, flag permanent life insurance policies owned by clients aged 65 or older with face values above $100,000. This should become a standard step in every annual review and estate planning meeting.

-

Gather policy documentation. Collect the policy illustration, in-force ledger, carrier statements, and any existing beneficiary designations. This documentation forms the basis of the settlement evaluation and helps establish current policy performance.

-

Engage a licensed life settlement broker. A qualified broker submits the policy to multiple institutional buyers simultaneously, creating a competitive bidding environment. This competition is what drives offers above surrender value. Asset Life Settlements manages this entire bidding process on behalf of advisors and their clients.

-

Compare the settlement offer to the surrender value. Once bids arrive, the comparison is straightforward: the settlement offer versus the carrier’s cash surrender value. Most clients are surprised by the gap. The difference represents real, recoverable wealth that would otherwise be abandoned.

-

Incorporate the settlement proceeds into the broader plan. This is where life settlement wealth planning becomes truly powerful. Settlement proceeds can fund a Roth conversion, seed a charitable remainder trust, cover long-term care costs, or simply add liquidity to an estate that is otherwise tied up in illiquid assets.

-

Document everything. Record the bids received, the client’s decision, and the rationale for the chosen path. This documentation protects advisors from fiduciary challenges and creates a clear audit trail.

Pro Tip: Never present a life settlement as the default recommendation. Present it as one option in a thorough policy review. The goal is informed decision-making, not steering. Clients who understand their options make better choices and trust their advisors more.

If no competitive bids materialize, the evaluation adds due diligence without any downside. The policy is surrendered as planned, and the advisor has fulfilled their fiduciary obligation.

Common mistakes when adding life settlements to wealth transfer strategies

Even experienced advisors stumble in predictable ways when incorporating settlements in estate planning. Knowing these pitfalls in advance saves clients real money.

The most widespread problem is not a regulatory gap. Lack of advisor training, not regulation, is the primary barrier to life settlement adoption. Many advisors were trained at large firms that actively discouraged the conversation because policy lapses benefit carriers financially. That institutional bias has quietly cost policyholders billions in recoverable value.

Here are the most common mistakes to avoid:

-

Skipping the evaluation entirely. Advisors who surrender or lapse policies without exploring settlement options expose clients to unnecessary asset loss and themselves to fiduciary risk.

-

Waiting too long. Once a policy has lapsed, the opportunity is gone. The evaluation must happen before the surrender decision is finalized.

-

Underestimating client interest. Many seniors assume their only options are to keep paying or walk away. Policy owners often miss the higher-value settlement option simply because no one raised it.

-

Ignoring premium financed policies. These require special attention. As one analysis notes, loan maturity and collateral calls can destabilize a wealth transfer plan well before death, making settlement evaluation even more time-sensitive.

-

Failing to document the conversation. Whether the client pursues a settlement or not, the advisor’s notes should reflect that the option was presented and considered.

“Fiduciary duty under the CFP Board Code and the Investment Advisers Act requires raising the life settlement option to protect client interests. Not raising it risks both asset value and professional standing.” Source

Life settlements are also not the right choice in every situation. If the insured still needs the death benefit for income replacement, a surviving spouse’s security, or a specific estate tax strategy, surrendering that coverage may not be appropriate. The goal is always the best outcome for the client, not the largest transaction.

What clients gain when life settlements are part of the plan

The tangible benefits of using life settlements for legacy planning go well beyond a one-time cash payment. When properly integrated, they reshape the efficiency of an entire wealth transfer strategy.

Life insurance and life settlements are increasingly integrated into outcome-focused retirement strategies alongside annuities and other income vehicles. The result is a more complete picture of client assets and a more intentional allocation of resources.

Specific benefits your clients can expect include:

-

Increased liquidity. Settlement proceeds convert an illiquid insurance asset into cash that can be deployed immediately, whether for healthcare, housing, or legacy gifts.

-

Reduced premium burden. Seniors who can no longer comfortably afford premiums gain relief without simply abandoning the policy’s value.

-

Enhanced wealth transfer efficiency. Proceeds can be redirected into vehicles better suited to the client’s current estate goals, such as irrevocable trusts or direct gifting strategies.

-

Real-time legacy impact. One compelling example from Asset Life Settlements’ own case history: a senior couple used settlement proceeds to give while living, funding family gifts and charitable contributions rather than waiting for the death benefit to transfer.

-

Estate tax planning flexibility. Liquid assets are easier to position around estate tax thresholds than illiquid insurance contracts, giving planners more room to work.

After the settlement closes, advisors should track how the proceeds are deployed, confirm beneficiary designations on any new vehicles, and revisit the overall plan within 12 months. The settlement is a transaction. The planning work that follows is what creates lasting value.

My take: why this evaluation should be standard practice

I’ve spent years watching advisors do thorough, thoughtful work on every dimension of a client’s financial life and then completely skip the policy review step before a surrender. It’s not negligence. It’s a training gap that the industry has been slow to close.

The uncomfortable truth is that many advisors were shaped by firms where life settlements were simply not discussed. Lapses were treated as natural outcomes. The idea that a client could sell that policy for meaningful cash never entered the conversation. That gap has cost real people real money, and in my view, it represents a genuine failure of the fiduciary standard.

What I’ve learned is this: adding a policy review step costs almost nothing and carries no downside risk. If no bids come in, you surrender as planned. If bids do come in, your client has options they didn’t know existed. That asymmetry makes the evaluation one of the most defensible steps in any wealth transfer plan.

I also think advisors underestimate how much clients appreciate being told about this option. It signals that you are looking out for every dollar, not just the ones that generate obvious fees. That kind of advocacy builds trust that lasts well beyond a single transaction.

Death is not the only relevant outcome in policy evaluation, and treating it as such leaves too much value unexamined. The best advisors I’ve seen treat every policy as a living asset with options, not a contract waiting to pay out.

— Scott Thomas

Work with Asset Life Settlements to get this right

If you’re ready to include life settlement in a wealth transfer plan for your clients, Asset Life Settlements gives you the tools and expertise to do it properly.

Asset Life Settlements is a licensed broker that manages the entire evaluation and bidding process on your behalf, from initial policy eligibility review to final settlement. Their track record includes securing a full $2 million for an 85-year-old client in a challenging market. You can start with their life settlement calculator to estimate potential value, or connect directly with their team to begin a formal evaluation. For financial professionals looking to build this into their practice, the resources for advisors page is the right starting point.

FAQ

What is a life settlement in wealth transfer planning?

A life settlement is the sale of an existing life insurance policy to a third-party buyer for more than its surrender value. In wealth transfer planning, it converts an underperforming policy into liquid capital that can be redeployed into more effective estate planning vehicles.

Which policies qualify for a life settlement?

Permanent life insurance policies with face values above $100,000, owned by insureds aged 65 or older, are the most common candidates. Declining health can expand eligibility to younger insureds or smaller policies.

Does exploring a life settlement carry any financial risk?

No. If no competitive bids are received during the evaluation, the policy can simply be surrendered as originally planned. The review adds a layer of due diligence without any cost or obligation to the policyholder.

Is a financial advisor required to mention life settlements?

Under the CFP Board Code and the Investment Advisers Act, fiduciary duty requires advisors to raise the settlement option to protect client interests. In six states, disclosure before lapse or surrender is legally mandated.

How do settlement proceeds fit into a broader wealth transfer strategy?

Proceeds can fund Roth conversions, charitable trusts, direct gifting, long-term care costs, or annuity purchases. Working with a financial planner, life insurance as a retirement asset can be repositioned to better match a client’s current goals rather than the objectives that existed when the policy was originally purchased.