Most people shopping for life insurance assume all policies build some kind of savings component over time. That assumption is wrong for the majority of term life insurance buyers, and acting on it can lead to serious financial planning mistakes. So, do term life insurance policies have cash value? The short answer is no. Standard term policies are designed as pure death benefit protection, with no cash accumulation component attached. Understanding this distinction before you buy protects you from surprises later and helps you choose the right coverage for your actual financial goals.

Table of Contents

- Key takeaways

- Do term life insurance policies have cash value?

- Why standard term policies have no cash value

- Exceptions worth knowing about

- Practical decisions about cash value and your coverage

- My perspective on cash value confusion

- How Asset Life Settlements can help you

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Term life has no cash value | Standard term life insurance policies do not accumulate cash value at any point during the policy term. |

| Permanent policies build cash value | Whole life and universal life policies include a cash value component that grows over time and can be accessed while you are alive. |

| ROP policies are the exception | Return-of-premium term policies refund premiums at the end of the term but are rare and more expensive than standard term coverage. |

| Life settlements offer an alternative | Selling a term policy through a life settlement can convert your death benefit into immediate cash, even without internal cash value. |

| Read your contract carefully | The cash surrender value section of your policy contract will confirm whether any cash value exists in your coverage. |

Do term life insurance policies have cash value?

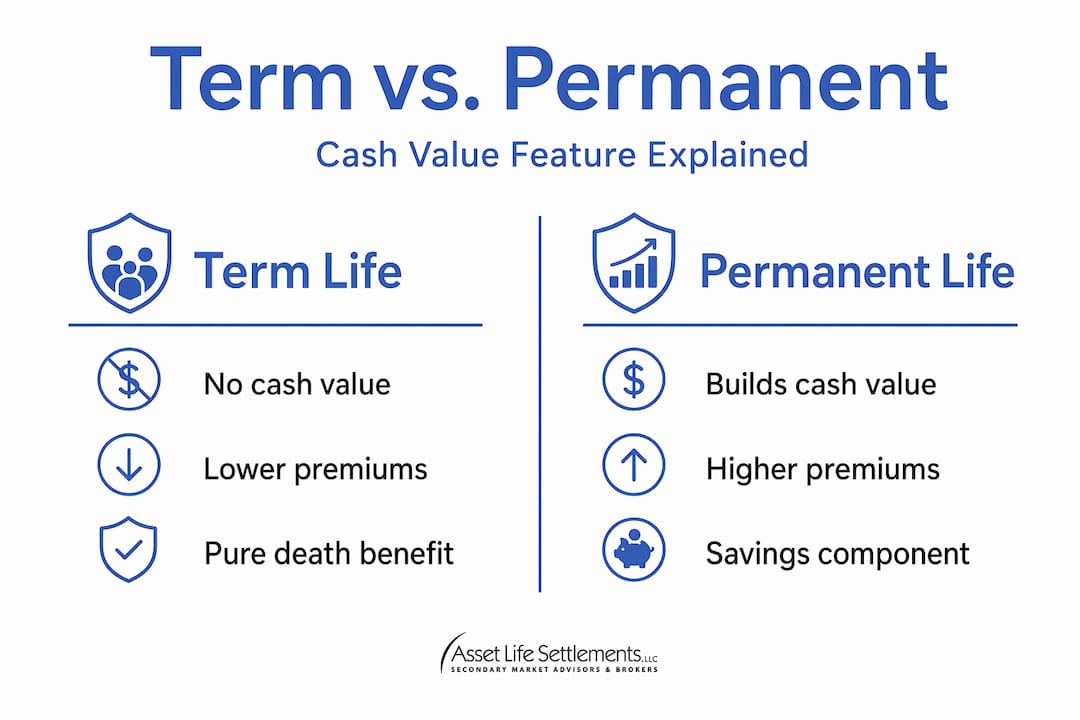

The industry term for the savings feature found in some life insurance products is "cash surrender value," or CSV. It represents the amount a policyholder can receive if they cancel their policy before it matures or before they pass away. Term life lacks cash value, while whole life policies include a cash value component that grows alongside the death benefit.

Here is how cash value works in the policies that do include it:

- Permanent life insurance products like whole life and universal life are the two main types that build cash value.

- Premium allocation: A portion of every premium payment goes toward the death benefit, while another portion funds the cash value account.

- Tax-deferred growth: All permanent policies come with a cash value component that grows on a tax-deferred basis over the life of the policy.

- Living benefits: Policyholders can borrow against the cash value, make withdrawals, or use it to pay future premiums while the policy remains active.

- Surrender charges: If you cancel a whole life policy early, you may owe surrender charges on cancellation, which reduce your payout. Term policies avoid this entirely because there is nothing to surrender.

A term policy has no cash account attached. Your premiums buy pure death benefit protection for a fixed period, such as 10, 20, or 30 years. When the term ends, the coverage ends. Nothing accumulates. Nothing gets paid out if you outlive the term.

Pro Tip: If you want to verify whether your current policy builds cash value, locate the "cash surrender value" section of your policy contract. Its absence confirms you have a traditional term policy with no accumulated savings component.

Why standard term policies have no cash value

Term life insurance is intentionally designed without cash accumulation. That design choice is the primary reason term premiums are dramatically lower than permanent policy premiums for the same death benefit amount.

Think about what you are actually purchasing. A 35-year-old buying a $500,000, 20-year term policy is paying for the insurer's promise to pay $500,000 if they die within those 20 years. That is it. No savings account. No investment component. No loan feature. Just coverage.

Here is why this matters for your wallet:

- Lower premiums: Because none of your payment goes toward building a cash reserve, the insurer can price the policy based purely on the mortality risk. Term's pricing structure reflects this directly, making it substantially more affordable than whole life for most buyers.

- No cash surrender value listed in your contract: Policy contracts explicitly state whether a cash surrender value exists. Nearly all term policies state no cash surrender value, which is the contractual confirmation that no cash benefit applies.

- No policy loans available: Because there is no cash pool built up within the policy, you cannot borrow against it. Permanent policyholders use this feature for emergency funds or retirement income supplements. Term policyholders have no equivalent option.

- No withdrawal option: You cannot cash in a term life insurance policy mid-term and walk away with money. If you stop paying premiums, coverage simply lapses.

The tradeoff is straightforward. You give up the living benefits of cash value in exchange for significantly lower premiums. For many people, especially those with young families and tight budgets, that tradeoff makes complete sense.

Stat to know: Misunderstanding the cash value feature is one of the most common sources of unrealistic expectations among term life policyholders, often leading to financial planning errors down the line.

Exceptions worth knowing about

Not every term-adjacent product behaves identically. Two situations create nuances worth understanding before you assume all term policies are the same.

Return-of-premium term policies

Return-of-premium (ROP) term insurance is a product variation that refunds 100% of premiums paid if you outlive the policy term. That refund can look and feel like cash value accumulation, but it works differently.

Here is how ROP compares to standard term and whole life coverage:

| Feature | Standard term | ROP term | Whole life |

|---|---|---|---|

| Death benefit | Yes | Yes | Yes |

| Cash value growth | No | No (premium refund only) | Yes |

| Premiums | Low | Higher | Much higher |

| Access to funds during term | No | No | Yes (loans/withdrawals) |

| Payout if you outlive term | Nothing | Full premium refund | Cash surrender value |

ROP policies are uncommon and few insurers offer them. The premiums can be 30% to 50% higher than standard term coverage. Whether the premium refund justifies the cost depends entirely on your financial situation and time horizon.

Life settlements as an alternative

If you own a term policy and need cash, there is one route worth knowing. A life settlement allows you to sell your policy to a third-party buyer for more than the surrender value and less than the death benefit. Selling a term policy through a life settlement is a potential way to access funds even though the policy itself has no internal cash value.

This option applies specifically to convertible term policies, where the term coverage can first be converted to a permanent policy. Once converted, the permanent policy becomes eligible for a life settlement. This is a more complex path, but it is a legitimate option for the right policyholder.

Pro Tip: If your term policy includes a conversion rider, that rider may be your most valuable asset. Conversion rights allow you to shift to a permanent policy without new medical underwriting, which then opens the door to life settlement consideration. Learn more about your policy exit options before assuming your term policy has no remaining value.

Practical decisions about cash value and your coverage

So do all life insurance policies have cash value? No. And knowing that fact is only useful if you apply it to your own decision-making process.

Here are the key questions to ask yourself before choosing between term and permanent coverage:

- Do you need living access to funds? If the ability to borrow against your policy or make withdrawals is a priority, permanent life insurance is the product designed for that purpose. Term life cannot serve that function.

- What is your budget? Term life allows you to carry a substantial death benefit for a fraction of the premium cost. A healthy 40-year-old can often secure $1 million in term coverage for less than $100 per month. Comparable whole life coverage would cost several times more.

- How long do you need coverage? Term life makes sense for time-bound needs. Covering a mortgage, protecting dependents while children are young, or replacing income during working years are all well-suited to term coverage.

- Are you using life insurance as part of a wealth-building strategy? Cash value in permanent policies can supplement retirement income or serve as a tax-advantaged savings vehicle for high earners who have maxed out other options. For most people, though, this is a secondary consideration.

- Have you read your policy contract? This point matters more than most people realize. The cash surrender value section tells you definitively whether your current coverage builds any value. Many policyholders have never reviewed this section.

Understanding term life insurance basics makes it easier to align your coverage choice with your actual financial situation rather than assumptions about how policies work.

My perspective on cash value confusion

I have seen the cash value misconception create real problems for real people. Clients who spent years believing their term policy was building a nest egg, only to discover at renewal time that there was nothing there. That confusion is not their fault. It is the result of vague marketing language and well-meaning advice that glosses over the structural differences between policy types.

What I have learned is that the question "can you cash in a term life insurance policy?" should be answered honestly and early, not when someone is already in a financial bind. The answer for standard term is no. And that is fine. Term coverage does exactly what it promises to do: it protects your family if you die during the covered period. That has genuine, meaningful value. It just does not double as a savings account.

Where I see the most damage is when permanent coverage is dismissed as "too expensive" without a real conversation about whether cash value features align with someone's long-term goals. And equally, when term policies are sold with an implied promise of financial flexibility that the product simply cannot deliver.

My advice: get clear on what you need the policy to do. If pure death benefit protection fits your budget and your timeline, term is excellent coverage. If you want a policy that works for you while you are still alive, then a permanent product or a life settlement strategy deserves serious consideration.

— Scott Thomas

How Asset Life Settlements can help you

If you are holding a term or permanent life insurance policy and wondering whether it still serves your financial needs, there are more options available than most policyholders realize.

Asset Life Settlements specializes in helping policyholders and their financial advisors evaluate whether a life settlement could unlock real value from an existing policy. Even when a term policy has no internal cash value, conversion and settlement strategies may put cash in your hands when you need it most. Asset Life Settlements has secured outcomes like a full $2 million settlement for an 85-year-old client even in difficult market conditions. That kind of result comes from experience, an extensive buyer network, and a transparent process built around your interests. Explore the life settlement process to understand exactly how a policy evaluation works and what you could potentially receive. You can also use the settlement value calculator to get an early estimate for your situation.

FAQ

Does term life insurance build cash value?

No. Standard term life insurance does not build cash value. It is designed as pure death benefit protection, and premiums pay only for that coverage with no savings component attached.

Can you cash in a term life insurance policy?

You generally cannot cash in a standard term policy because there is no accumulated cash to withdraw. The one exception is if your policy is convertible and you pursue a life settlement after converting to a permanent policy.

What types of life insurance build cash value?

Permanent life insurance policies, including whole life and universal life, build cash value over time. A portion of each premium funds a cash account that grows on a tax-deferred basis and can be accessed through loans or withdrawals.

What is a return-of-premium term policy?

A return-of-premium term policy refunds 100% of premiums paid if you outlive the term. While this resembles cash value accumulation, premiums are significantly higher and there is no access to funds during the active term.

Can a life settlement help term life policyholders access cash?

Yes, in certain cases. If your term policy includes a conversion rider, you may convert it to a permanent policy and then sell it through a life settlement. This can provide immediate cash even though the original term policy had no internal cash value.